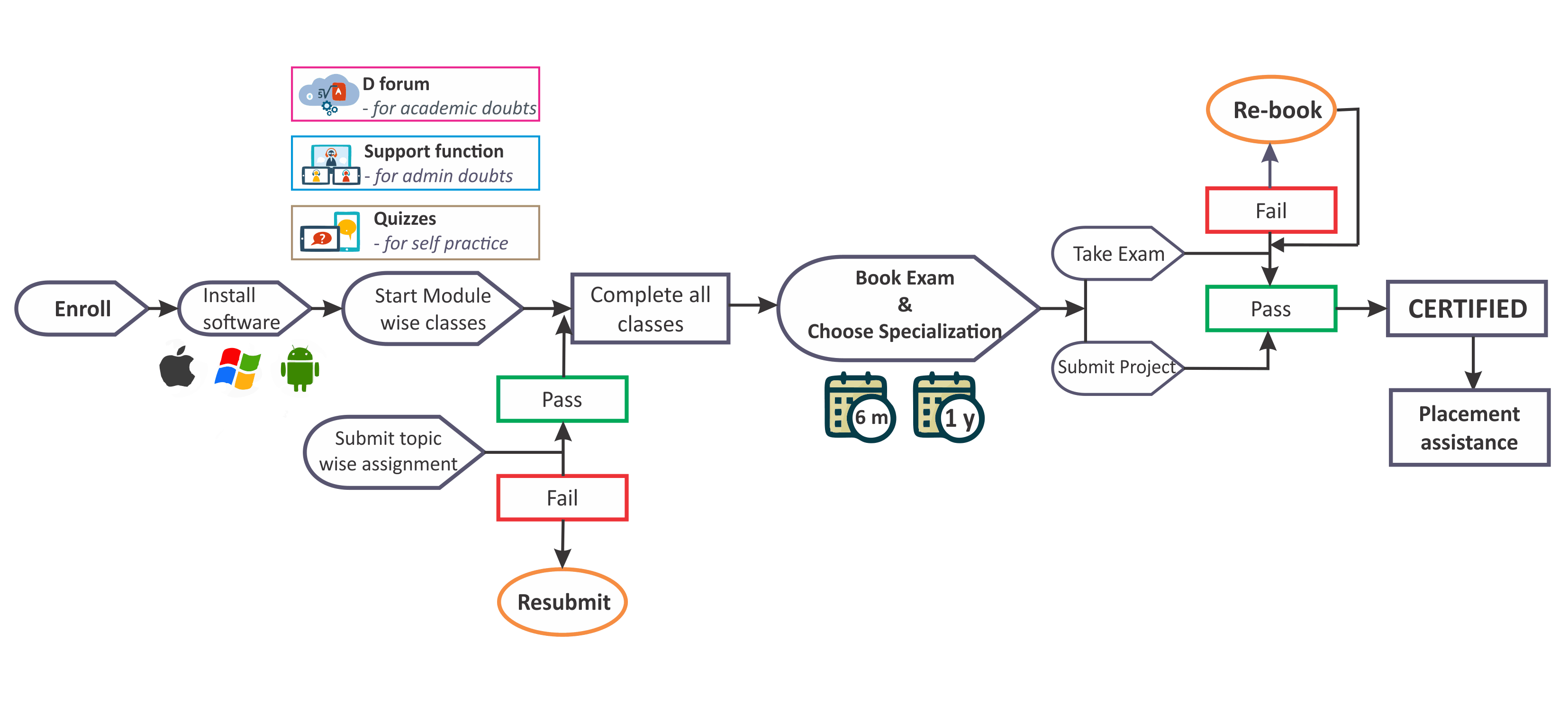

BOOTCAMP Credit Risk Modelling Platinum

No content

| Platinum Package = Gold Package + Live Masterclasses & Python Modelling | |

| Live Masterclasses 1 | |

| Integrated Credit Risk (15 hours) | |

| 01 | Application Scorecard and accept/reject decision |

| 02 | Credit Scorecards using WOE binning and rating assignment based on Master Rating Scale |

| 03 | Understanding of RWA and Capital calculation under Internal Rating Based approach |

| 04 | Computation of PD using Vasicek formula |

| 05 | Computation of LGD using Chain Ladder Method |

| 06 | Computation of Point in time PD and Point in time LGD using Z score and Jacob Frye |

| 07 | Computation of 1 year and lifetime expected credit losses |

| 08 | Computation of Stressed Losses under ICAAP |

| 09 | Loan Pricing using RAROC concepts |

| Live Masterclass 2 | |

| Expected Credit Loss under IFRS 9 and stress testing (15 hours) | |

| 01 | Snapshot & Performance Window creation |

| 02 | Preparing Macro Economic Variables |

| 03 | Building TTC Logistic Regression Model |

| 04 | Building PIT Logistic Regression Model |

| 05 | Validating Discriminatory Power for each Snapshot |

| 06 | Performing Backtesting/Bias/Error analysis over different performance periods. |

| 07 | Building Stress testing model and Validating the results |

| 07 | Benchmarking model results with Z score and other calibration techniques |

| Live Masterclass 3 | |

| Credit Abhyaas (15 hours) | |

| 01 | Validating Scorecards |

| 02 | Validating IRB PD/IRB LGD/IRB EAD models |

| 03 | Valifating Staging and SICR criteria |

| 04 | Validating ECL models |

| 05 | Validating Stress Testing models |

| 06 | Validating Low default portfolios |

| 07 | Qualitative validation |

| 08 | SR 11-7 principles |

| 02 | 12 months PD calculation vs lifetime PD calculation |

| 03 | Understanding Concepts of Staging – Stage 1| Stage 2 | Stage 3 |

| Python Modelling hand-on (50 hours) | |

| 01 | Data Preparation techniques |

| 02 | Linear Regression |

| 03 | Time Series |

| 04 | Logistic Regression |

| 05 | General linear models |

| 06 | Behavioural Scorecard PD |

| 07 | LGD Models |

| 08 | EAD Models |

| 09 | Validation of PD model |

| 10 | Validation of LGD and EAD models |

| 11 | Building IFRS 9 ECL model |

| 12 | Building Stress Testing Models |

| 13 | Building IFRS 9 models for Wholesale using Transition Matrices |

| 14 | Building Application Scorecard |

ABOUT THE TRAINER

No content

No content

| Platinum Package = Gold Package + Live Masterclasses & Python Modelling | |

| Live Masterclasses 1 | |

| Integrated Credit Risk (15 hours) | |

| 01 | Application Scorecard and accept/reject decision |

| 02 | Credit Scorecards using WOE binning and rating assignment based on Master Rating Scale |

| 03 | Understanding of RWA and Capital calculation under Internal Rating Based approach |

| 04 | Computation of PD using Vasicek formula |

| 05 | Computation of LGD using Chain Ladder Method |

| 06 | Computation of Point in time PD and Point in time LGD using Z score and Jacob Frye |

| 07 | Computation of 1 year and lifetime expected credit losses |

| 08 | Computation of Stressed Losses under ICAAP |

| 09 | Loan Pricing using RAROC concepts |

| Live Masterclass 2 | |

| Expected Credit Loss under IFRS 9 and stress testing (15 hours) | |

| 01 | Snapshot & Performance Window creation |

| 02 | Preparing Macro Economic Variables |

| 03 | Building TTC Logistic Regression Model |

| 04 | Building PIT Logistic Regression Model |

| 05 | Validating Discriminatory Power for each Snapshot |

| 06 | Performing Backtesting/Bias/Error analysis over different performance periods. |

| 07 | Building Stress testing model and Validating the results |

| 07 | Benchmarking model results with Z score and other calibration techniques |

| Live Masterclass 3 | |

| Credit Abhyaas (15 hours) | |

| 01 | Validating Scorecards |

| 02 | Validating IRB PD/IRB LGD/IRB EAD models |

| 03 | Valifating Staging and SICR criteria |

| 04 | Validating ECL models |

| 05 | Validating Stress Testing models |

| 06 | Validating Low default portfolios |

| 07 | Qualitative validation |

| 08 | SR 11-7 principles |

| 02 | 12 months PD calculation vs lifetime PD calculation |

| 03 | Understanding Concepts of Staging – Stage 1| Stage 2 | Stage 3 |

| Python Modelling hand-on (50 hours) | |

| 01 | Data Preparation techniques |

| 02 | Linear Regression |

| 03 | Time Series |

| 04 | Logistic Regression |

| 05 | General linear models |

| 06 | Behavioural Scorecard PD |

| 07 | LGD Models |

| 08 | EAD Models |

| 09 | Validation of PD model |

| 10 | Validation of LGD and EAD models |

| 11 | Building IFRS 9 ECL model |

| 12 | Building Stress Testing Models |

| 13 | Building IFRS 9 models for Wholesale using Transition Matrices |

| 14 | Building Application Scorecard |

No content